Palomar officials are implementing measures to stop the college’s streak of deficit spending.

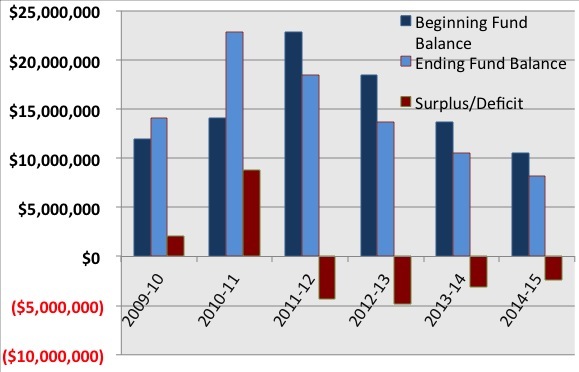

Since 2011, Palomar has dipped into its Ending Fund Balance, which is the amount of money the college has leftover from a fiscal year, to pay for various expenditures. The balance has dropped from $18.4 million to about $8 million.

The college staff has several cost cutting initiatives planned, including the Supplemental Employee Retirement Program, also known as a “golden handshake.” The SERP is offering an incentive for employees who want to retire early.

The SERP is expected to save the district about $2.7 million, according to Ron Perez, vice president of finance and administrative services.

College officials are also looking at moving their health care services to another firm, which would save them around $600,000 to $1 million a calendar year.

Palomar is also reworking their enrollment management, which is essentially cutting classes with lower enrollment numbers and increasing class sections with a higher demand.

Palomar receives much of its funding from the state, according to how many full-time students are enrolled. The higher the number of credit hours taken, the more money Palomar is allocated.

From 2010 to 2012, the state went through a budget crisis that forced them to cut funding for colleges across California. The college started deficit spending to avoid layoffs of faculty and staff, salary pay cuts or requiring staff to pay for health care.

“We actually offered more classes than what the state gave us money for,” Perez said. “So we used our ending fund balance to offer those additional class sections.”

The school was “way underfunded” for the classes they offered, according to Phyllis Laderman, director of Fiscal Services.

Perez said that to meet the needs of students, it’s preferable to have more unfunded FTES if the college has the finances to cover it.

Perez stated that the college’s fiscal future is looking good, but that “we’re not out of the woods yet.”